Why How You *Think* About Debt Matters

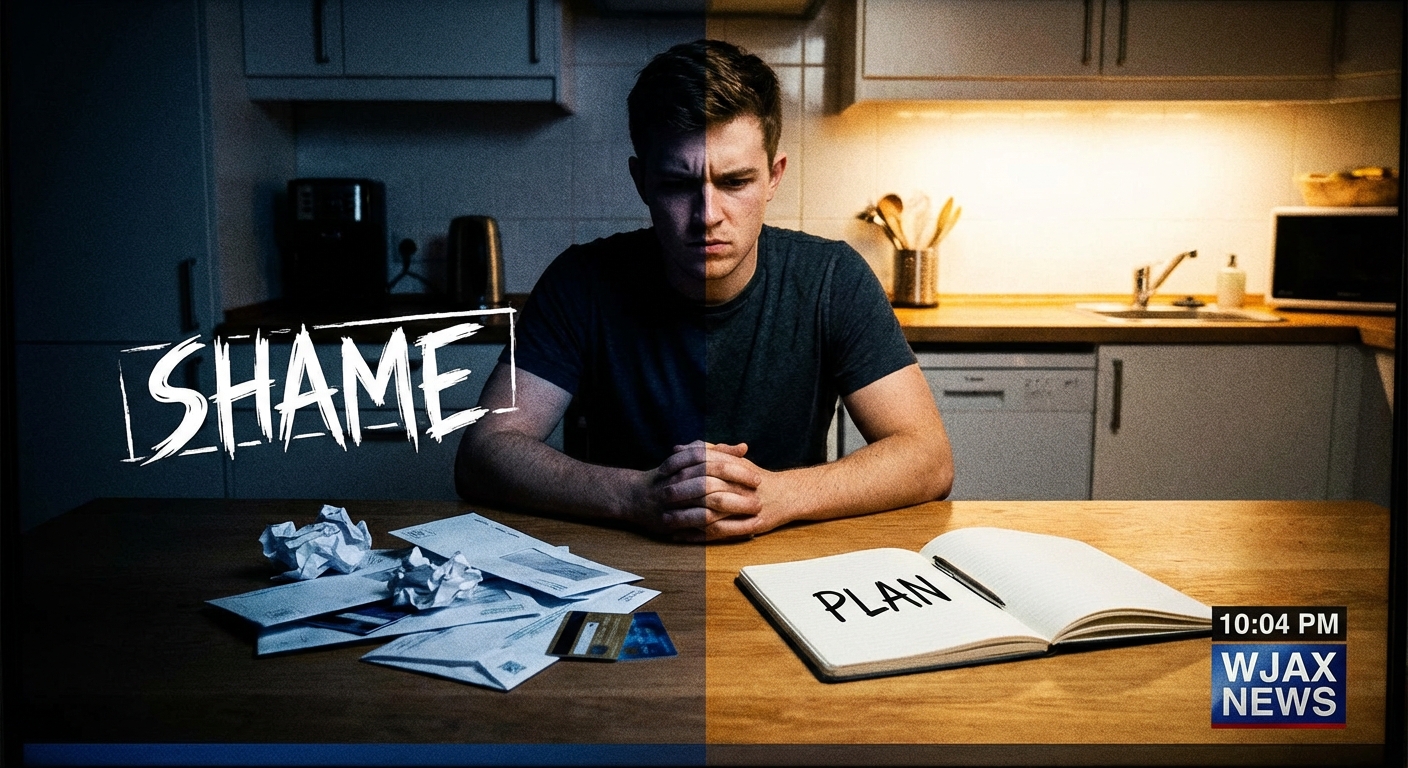

Owing money can feel heavy. Many people carry not just balances, but **shame**:

- "I’m stupid for getting into this much debt."

- "I’ll never get out from under this."

- "I messed up my life."

Shame doesn’t pay off a single dollar. What actually helps is a **strategy**—and a mindset that sees debt as a problem to be solved, not a personal failure.

This article will help you:

- Understand common unhelpful beliefs about debt

- See real, simple examples of debt payoff strategies

- Practice kinder self-talk that keeps you motivated

- Take concrete first steps—even if your debt feels overwhelming

You don’t need to be perfect, and you’re not alone.

---

Step 1: Separate Your Self-Worth From Your Debt Number

Debt is a **number**, not your identity.

A credit card balance of $4,800 doesn’t mean you’re lazy, reckless, or broken. It means that at some point, you used borrowed money. This may have been because of:

- Low income

- Lack of savings

- Medical bills

- Job loss

- Family responsibilities

- Gaps in financial education

Most of these are **system problems**, not personal flaws.

Try this small mental shift:

Instead of:

> "I am bad with money."

Say:

> "I currently have $X of debt. I’m learning how to handle it better."

The situation is the same, but the second version leaves room for improvement.

---

Step 2: Turn the Messy Pile Into a Clear List

Shame thrives in vagueness—"a ton of debt," "so many bills." Strategy starts with **real numbers**.

What to Gather

List each debt with:

1. **Type:** (credit card, student loan, car loan, personal loan, etc.)

2. **Balance:** How much you currently owe

3. **Interest rate (APR):** The yearly cost to borrow, in percentage

4. **Minimum payment:** What you must pay each month

If you’re not sure of the rate or balance, log in to your account or call the lender. It’s okay if this feels scary. Take it one account at a time.

Example Debt List

Let’s say you write this down:

1. Credit Card A

- Balance: $1,200

- APR: 24%

- Minimum payment: $36

2. Credit Card B

- Balance: $600

- APR: 19%

- Minimum payment: $25

3. Car Loan

- Balance: $7,000

- APR: 7%

- Minimum payment: $210

Your **total debt**: $8,800

Now the problem is defined, which means we can work with it.

---

Step 3: Choose a Simple Payoff Strategy (With Real Numbers)

There are many methods, but for beginners, two are especially useful:

1. **Debt Snowball:** Focus on the **smallest balance first**

2. **Debt Avalanche:** Focus on the **highest interest rate first**

We’ll walk through both using the example above, assuming you can put **$320/month** toward all debts combined.

Option 1: Debt Snowball (Smallest First)

Order by balance:

1. Card B – $600 (19%)

2. Card A – $1,200 (24%)

3. Car Loan – $7,000 (7%)

Steps:

- Pay minimums on all except Card B.

- Put every extra dollar toward Card B.

Numbers:

- Minimums: Card A $36 + Card B $25 + Car $210 = $271

- Extra available: $320 – $271 = $49

You pay to Card B:

- $25 (minimum) + $49 (extra) = **$74/month**

Rough estimate: Card B gone in about **9 months** (ignoring small interest changes).

Once Card B is gone:

- Roll that $74 into Card A: $36 + $74 = **$110/month**

This method gives you **quick wins** (one less bill), which often boosts motivation.

Option 2: Debt Avalanche (Highest Interest First)

Order by APR:

1. Card A – 24% (Balance $1,200)

2. Card B – 19% (Balance $600)

3. Car Loan – 7% (Balance $7,000)

Steps:

- Pay minimums on all except Card A.

- Put every extra dollar toward Card A.

Numbers:

- Minimums: Card A $36 + Card B $25 + Car $210 = $271

- Extra available: $320 – $271 = $49

You pay to Card A:

- $36 (minimum) + $49 (extra) = **$85/month**

Card A would be paid off **faster** than Card B in the snowball method, and you pay **less interest overall.**

However, some people find the avalanche method emotionally harder if their highest-interest debt also has the biggest balance.

Which Is “Right”?

The best method is the one you’ll **stick with**.

- If you need quick emotional wins → Snowball.

- If you’re highly motivated by math and saving interest → Avalanche.

Choosing any intentional method is a huge mindset win.

---

Step 4: Reframe Minimum Payments as a Beginning, Not the Goal

Minimum payments keep your account in good standing—but they’re often designed to stretch debt out for years.

Shame says:

> "I can only afford the minimum. I’m failing."

Strategy says:

> "Right now, I can pay the minimum. I’ll look for ways to add even $5–$20 when I can."

The Power of Small Extras

Take Card A from the example:

- Balance: $1,200

- APR: 24%

- Minimum: $36

A rough illustration (not exact):

- Paying only $36/month could take **4+ years** and cost hundreds in interest.

- Paying **$56/month** ($20 extra) might cut that significantly.

Even if $20 feels like a lot, **$5–$10 extra** still helps. The mindset shift is:

> "Any extra money I send to debt is me buying back my future income."

You’re not just paying a bill; you’re freeing up tomorrow’s paycheck.

---

Step 5: Practice Neutral, Not Nasty, Self-Talk

Your inner voice during this process matters. Harsh self-talk leads to avoidance and giving up.

Replace statements like:

- "I ruined everything."

- "I’m so stupid with money."

With neutral versions:

- "I made decisions with the information and options I had at the time."

- "I can’t change the past, but I can change how I handle this debt now."

A Simple Script for Tough Days

When you feel overwhelmed by debt, try saying:

> "This number feels big, and I am allowed to take this one step at a time. Today, I’ll focus on [tiny action]."

Tiny actions can be:

- Paying $5 extra

- Calling a lender to ask about hardship options

- Updating your debt list with current balances

---

Step 6: Give Your Debt a Clear Role in Your Plan

Debt feels scarier when it’s a vague dark cloud. It feels more manageable when it has a **role** in your overall money picture.

A simple way to structure your plan:

1. **Survival:** Pay all minimums on time.

2. **Stability:** Build a tiny emergency fund so you don’t add more debt.

3. **Momentum:** Focus extra money on one targeted debt at a time.

Example on $2,200 Take-Home Income

Let’s say:

- Needs (rent, food, utilities, etc.): $1,400

- Minimum debt payments: $300

- Total so far: $1,700

You have $500 left.

You might choose:

- $100 → Starter emergency fund (until you reach $300–$500)

- $150 → Extra payment on target debt

- $250 → Wants (fun, small treats, clothing, etc.)

This way:

- You’re preventing **new** debt by building a small cushion.

- You’re reducing **old** debt with consistent extra payments.

- You still have room for life so you don’t burn out.

---

Step 7: Use Support, Not Secrecy

Shame tells you to hide. Strategy often needs support.

Possible sources of help:

- **Trusted friend or partner:** Share your goal and celebrate milestones together.

- **Nonprofit credit counseling agencies:** Many offer free or low-cost sessions. They can help you:

- Review your debts

- Create a realistic budget

- Sometimes negotiate lower rates or a structured repayment plan

- **Supportive online communities:** Look for spaces focused on encouragement and learning, not shaming.

You control what you share. You don’t have to give every detail. Even saying to someone, "I’m working on my debt and trying to make better choices" can reduce isolation.

---

Step 8: Redefine Success Along the Way

Success with debt is not just "zero balance or failure." Celebrate steps like:

- Listing all your debts

- Making your first extra payment

- Paying off your smallest account

- Calling a lender instead of avoiding it

- Going one full month without adding new debt

Each is a sign that your mindset is shifting from **debt shame** to **debt strategy.**

---

A Gentle 30-Day Debt Mindset Plan

If you want a clear starting path, try this:

**Week 1** – Awareness

- List all debts with balances, APRs, and minimums.

- Practice one neutral self-talk script whenever shame pops up.

**Week 2** – Strategy

- Choose snowball or avalanche.

- Decide how much total you can send to debt each month.

**Week 3** – Action

- Make your first targeted extra payment—even if it’s $5.

- Look for one small way to free $10–$20/month (subscription, small habit change).

**Week 4** – Support & Review

- Tell one trusted person you’re working on your debt.

- Review your balances and acknowledge any progress.

---

You Are Not Your Debt

Your debt is **one part** of your financial life, not the whole story. You are also your effort, your learning, your resilience, and your future choices.

You don’t need to feel proud of your debt to start treating yourself with respect while you pay it down. In fact, self-respect is often what makes consistent progress possible.

Today, choose one step:

- Make a complete list of your debts, or

- Decide on snowball vs. avalanche, or

- Pay a tiny extra amount on one account.

That small action is you moving from debt shame to debt strategy—and that mindset shift is more powerful than you might think.